Abstract

The effective calculation of carbon emissions is critical for combating global warming. However, carbon accounting suffers from data quality issues, measurement and reporting inconsistencies, and digital infrastructure challenges. G20 members account for around 80 percent of global carbon emissions, and therefore, they can set standards in this domain for other countries to follow. A global standard for carbon accounting can provide a common framework for calculating emissions and opportunities for reduction. Scope 1, 2, and 3 emissions were developed to measure and report carbon footprint. Each category represents a different source of emissions, and each comes with its own set of challenges—from data collection and management, to lack of standardisation and accuracy. There is a broad recognition that the roadblocks to carbon accounting cannot be overcome by any country alone. Interoperability and transparency are key with the application of technologies.

The Challenge

The G20 Bali Leaders’ Declaration of 2022 noted that climate crises are compounded by geopolitical challenges, and the member states reiterated their commitment to achieving global net-zero greenhouse gas emissions by or around mid-century.1 In the same summit, the G20 members noted that “G20 climate policies, although improved and leading to slower growth in emissions, remain insufficient to meet the Paris Agreement.”2 The G20 Rome Leaders’ Declaration of 2021 also stated that member countries will further promote cooperation, improve data collection, verification, and measurement in support of GHG inventories and provide high-quality scientific data.3 In 2022, the United Nations took steps to hold investors, businesses, cities, and regions responsible for reducing GHG emissions, when UN secretary-general António Guterres asked an expert panel to develop standards for ‘net-zero’ pledges by these groups. The challenge is how to count emissions coherently.4 Owing to the inconsistent and frequently inaccurate nature of on-the-ground business and country-specific carbon disclosures, it is difficult to obtain a clear picture of climate effects and progress. For instance, just one-third of suppliers inform consumers about their indirect emissions, which causes businesses to report different levels of emissions for the same operations.5

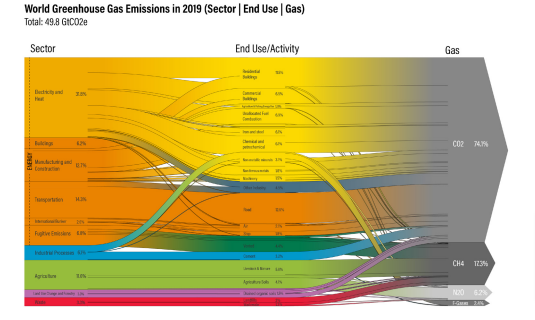

The United Nations Framework Convention on Climate Change (UNFCC, 1992) acknowledged that change in the Earth’s climate and its adverse effects are a common concern of humankind.6 Parties to the Convention committed to adopting national policies and take corresponding measures on the mitigation of climate change (UNFCC, 1992). Carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphur hexafluoride (SF6) are six greenhouse gases that are recognised to contribute to global warming (Kyoto Protocol).7 Of all GHG emissions, carbon dioxide (CO2) comprises 74.1 percent (see Fig. 1). (WRI, 2022)8

Figure1. Global Greenhouse Gas Emissions, 2019 (Sector I End Use I Gas)

Note: The figure describes the sources (sector: energy, industrials processes, agriculture, land use changes and forestry and waste); and activities/end use (anthropogenic); across the global economy that produce greenhouse gas (CO2, CH4, N2O and F-gases) emissions, as well as the type and volume of gases associated with each activity. Source: World Resources Institute.

Note: The figure describes the sources (sector: energy, industrials processes, agriculture, land use changes and forestry and waste); and activities/end use (anthropogenic); across the global economy that produce greenhouse gas (CO2, CH4, N2O and F-gases) emissions, as well as the type and volume of gases associated with each activity. Source: World Resources Institute.

This chart offers a comprehensive view of GHG emissions. It describes the sources and activities across the global economy that produce emissions, as well as the gas types and volumes associated with each activity.9 The energy sector accounts for the largest share of CO2, followed by agriculture, industrial processes, land use and forestry, and waste. Fig. 2 shows the annual CO2 emission of fossil fuel and industry, excluding CO2 emission due to land use change.10

Figure 2: Annual CO2 Emissions, by World Region

Source: Our World in Data

The largest carbon dioxide emitters among the G20 members were China, the United States, and the EU. Taking the number of inhabitants into account, the ranking shifts. The highest CO2 emissions per inhabitant of all G20 countries were recorded by Saudi Arabia, followed by Canada, Australia, and the United States. With around 8.7 tonnes, China’s per capita emissions were above the EU level of 6.3 tonnes.11

Figure 3: Top G20 Members, Carbon Dioxide Emissions Per Capita, 2021

Source: EDGAR/JRC, Statistisches Bundesamt, (Destatis) 2022

As nearly two-thirds of the world’s GHG emissions are accounted for by the G20, they are required to take meaningful action for the world to successfully combat climate change. This entails accurately measuring emissions.12

Standards and Protocols

Carbon accounting involves recognising, evaluating, and monitoring GHG emissions and their effects on ecosystems.13 The most commonly used standards for carbon accounting are Greenhouse Gases Protocol, ISO 14064, and IPCC Guidelines. However, some G20 members have raised concerns about certain indicators used by the UNFCCC and are seeking the inclusion of indicators aligned with the principle of ‘common but differentiated responsibilities’.14

The GHG Protocol is the first protocol developed for GHG accounting for both organisations and projects. It provides guidelines for companies to adopt when disclosing their carbon emissions. Scopes 1, 2, and 3 are used to classify emissions. Scope 1 considers direct GHG emissions from sources under the organisation’s ownership or control. Scope 2 takes into consideration the GHGs emissions produced by the organisation’s use of purchased electricity. All other indirect emissions may be handled under Scope 3, an optional reporting category. There are also three ISO 14064 standards relevant to GHG accounting: the ISO 14064 standards series I, II, and III, developed by the international standards organisation.16,17,18

While the ISO standards and the GHGs protocol are the most widely used resources in GHGs accounting, there are other resources such as the Environmental Protection Agency (EPA) Climate Leader Protocols, and the California Climate Action Registry, that support organisations in the area of GHG measurement and management.19,20, The IPCC has provided guidelines and methodologies for calculating GHG emissions and removals, including in the forestry and agriculture and industries.21 The 2019 Refinement report to the 2006 IPCC guidelines offers a methodology for creating national GHG inventories that covers various sectors such as energy, industrial processes, agriculture, waste, forestry, and other land.22 The global trend of increased GHG accounting and reporting places increased demand on companies to compile comparable and sharable GHG information.23 Regulators in various markets have implemented measures to require or incentivise companies to report environmental and carbon-related information.24

However, the practice of carbon accounting still faces several obstacles such as data quality issues, measurement and reporting inconsistencies, platforms that are in silos, and digital infrastructure challenges.25 Greenhouse gas estimates are subject to significant uncertainty, and most of the largest emitting events under Scope 3 are often difficult to include in inventories.28 Inconsistencies highlight the need for thorough and open data evaluation.27 Additionally, capturing Scope 3 emissions involves methodological difficulties, including tracking the carbon content of a product as it moves down the supply chain.29

Without addressing these problems, it is difficult to compare, combine, and share reliable data.29 The difficulty of tracking emissions from multiple suppliers and customers across multi-tier value chains makes it virtually impossible for a company to have a reliable estimate of its Scope 3 numbers.30 These roadblocks can hinder internal reliability and data exchange. To reach net-zero emissions for the world, global integrated reporting is crucial. Reporting rules that are interoperable across geographies such as the Task Force on Climate-Related Financial Disclosures (TCFD) can help in sustainability disclosure standards.31

The G20’s Role

Several reports have highlighted the importance of the G20 in the fight against climate change.32,33, For example, a 2021 report by the Climate Analytics and World Resources Institute titled “Closing the Gap: G20 Climate Commitments and Limiting Global Temperature Rise” found that G20 countries’ efforts to reducing emissions need to be ramped up to limit global temperature rise to 1.5°C above pre-industrial levels, as recommended by the Paris Agreement.34

The most relevant G20 working group for building consensus on global standards for carbon accounting is the Environment and Climate Sustainability Working Group (ECSWG). It is responsible for addressing issues related to energy, climate change, and the environment. Building consensus will require a strategic approach that involves developing coalition strategies, focusing on shared interests and collective responsibility, and forming sub-groups to address specific issues within ECSWG. There is need for a practical approach to the development of global standards for carbon accounting within the G20’s ECSWG: to convene a diverse group of stakeholders, identify existing standards and best practices, develop a common framework, pilot, and refine the framework, and establish mechanisms for ongoing review and improvement.

The G20 is the fit platform for the challenge of setting global standards for carbon accounting as it is composed of the world’s largest economies, accounting for over 80 percent of global GDP and approximately 80 percent of global carbon emissions. As such, the G20 has the ability to shape global economic policy and drive the adoption of new standards and practices in areas such as carbon accounting.

Currently, there is no universal standard for carbon accounting, which creates inconsistencies and challenges in comparing emissions data across countries and industries. Developing global standards for carbon accounting by the G20 would facilitate more accurate and transparent reporting of emissions data, which would, in turn, support the development and implementation of effective climate change mitigation strategies across the world.

A commitment to setting a global standard for carbon accounting by G20 members will create a world ecosystem that will support innovation and technological advancement in the carbon reporting field. This will also create an opportunity for the startup ecosystem to come up with scalable solutions in this space.

Recommendations to the G20

Enhance the accuracy of methodologies and the quality of the underlying data.

The prospects for and barriers to increasing the quality of source data, data products, calculation procedures, particularly for land, non-CO2 gases, offsets, and indirect emissions, must be evaluated by practitioners and researchers from across the world. A more long-term approach is to work with local partners and stakeholders to improve the quality and availability of carbon data in sectors and countries where it is lacking. This could include investing in data infrastructure to support new data collection efforts, and promoting data sharing among countries and organisations.

Create the standards and guidelines necessary for interoperability.

A GHGs ledger system must be created to promote institutional interoperability by creating a framework for cooperation and collaboration among different institutions involved in carbon accounting. Three groups of protocols are required.

- It is necessary to have technical and syntactic standards that outline how information should be interpreted by both humans and machines. For frictionless communication between ledgers, platforms, and data libraries, data must be structured and interoperable systems should be built to ensure the accuracy of greenhouse gas accounting. The suggested criteria for business sustainability reporting from the International Sustainability Standards Board could serve as a starting point.

- Improved definitions of the various metrics and terminology so that systems can communicate information without ambiguity. For matters like how uncertainty is measured, how offsets are categorised, and how emissions are divided across managed and uncontrolled lands, we require uniform and widely accepted taxonomy.

- The final requirement is for institutional interoperability protocols and concepts. These include laws and rules that make it easier for businesses and across borders to exchange data.

Build trust in GHG reporting through increased transparency.

Data on emissions, removals, and nation and company compliance with pledges should be made publicly available in a machine-readable, interoperable format. This could be done by compiling emissions data into a single global register or a network of sectoral and interoperable national registries.

Ensure that any solution takes both developed and developing countries’ demands into account.

Any global carbon accounting framework that is successful will need to be implemented locally by both the public and private sectors and should take into consideration technical capabilities at the national level. The opportunity to baseline need to be simple enough to encourage adoption by MSMEs.

Mass awareness and skill-building.

Every participant must comprehend what, why, and their place in the value chain for the standards alignment to be successful. Organisations and governments must work together to make sure that citizens have the tools necessary to track, report, and take deliberate steps to minimise their carbon emissions.

Build a Global Carbon Ratings Platform.

Governments and organisations can use carbon ratings as a tool to evaluate the environmental impact of their emissions. Carbon ratings must be founded on transparent procedures that accurately reflect the organisation’s or country’s emissions profile in order to be effective. By offering instructions on how to calculate emissions and creating a framework for evaluating carbon ratings, the G20 may contribute to the definition of carbon ratings. The key to success will depend on how ratings encourage the Global South to adopt decarbonisation, making sure that members can participate in it on an economic and technological level.

Boost decarbonisation with climate finance.

Climate finance can provide funding for mitigation and adaptation activities and can be linked to carbon ratings through a range of mechanisms, such as emissions trading schemes, carbon taxes, and renewable energy certificates. The G20 must reach an agreement to provide finance possibilities to encourage governments and corporations.

Encourage public-private partnerships.

Encouraging public-private partnerships is crucial for the development of innovative solutions. By leveraging resources and expertise from both sectors, these partnerships can drive new technology development, promote standardised reporting, and improve data quality. Strategies to promote such partnerships include financial incentives, collaboration frameworks, co-creation, and aligning incentives.

Attribution: Ravi Kumar Mahto, Srishti Saxena and Kaushal Mahan, “Global Standards for Carbon Accounting: An Agenda for G20,” T20 Policy Brief, May 2023.

Endnotes

1 “Bali Leaders’ Declaration,” G20, Bali, Indonesia, 2022,

2 G20, “Bali Leaders’ Declaration.”

3 “Rome Leaders’ Declaration,” G20, Rome, Italy, 2021.

4 Luers, Amy, Leehi Yona, Christopher B. Field, Robert B. Jackson, Katharine J. Mach, Benjamin W. Cashore, Cynthia Elliott, et al., “Make greenhouse-gas accounting reliable – build interoperable systems,” nature, 607, 2022, 653-656.

5 Klaaßen, L., Stoll, C., “Harmonizing corporate carbon footprints,” Nat Commun, 12, 6149 (2021).

6 “United Nations Framework Convention on Climate Change,” United Nations, 1992, Accessed February 21, 2023.

7 “Kyoto Protocol to the United Nations Framework Convention on Climate Change,” United Nations, 1998, Accessed March 11, 2023.

8 “World Greenhouse Gas Emissions in 2019 (Sector | End Use | Gas),” World Resource Institute, Accessed February 26, 2023.

9 World Resource Institute, “World Greenhouse Gas Emissions in 2019 (Sector | End Use | Gas).”

10 “Our World in Data”, annual CO2 emissions by world region, accessed March 13, 2023.

11 “G20 responsible for approximately 81% of global CO 2 emissions” Destatis Statistisches Bundesamt, Accessed March 20, 2023. G20 Carbon dioxide emissions – German Federal Statistical Office (destatis.de).

12 “Reporting and Review under the Paris Agreement,” Process and Meetings, UNFCCC.

13 Marlowe Jillene and Amelia Clarke, “Carbon Accounting: A Systematic Literature Review and Directions for Future Research,” Green Finance, 4(1), 2022, 71-87, https://www.aimspress.com/article/doi/10.3934/GF.2022004.

14 “Ministry of Environment, Forest and Climate Change Rebuts the Environmental Performance Index 2022 released recently,” Press Information Bureau, June 8, 2022, Accessed February 25, 2023, https://www.pib.gov.in/PressReleasePage.aspx?PRID=1832058.

15 “A Corporate Accounting and Reporting Standard,” The Greenhouse Gas Protocol, World Business Council for Sustainable Development: World Resource Institute, Accessed March 17, 2023, https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf.

16 “Greenhouse gases – Part I: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals,” ISO 14064-1:2018, International Organization for Standardization, Accessed March 18, 2023, https://www.iso.org/standard/66453.html.

17 “Greenhouse gases – Part II: Specification with guidance at the project level for quantification, monitoring and reporting of greenhouse gas emission reductions or removal enhancements,” ISO 14054-2: 2019, International Organization for Standardization, Accessed March 18, 2023, https://www.iso.org/standard/66454.html.

18 “Greenhouse gases — Part 3: Specification with guidance for the verification and validation of greenhouse gas statements,” ISO 14064-3:2019, International Organization for Standardization, Accessed March 18, 2023, https://www.iso.org/standard/66455.html.

19 “GHG Inventory Guidance”, EPA, United States Environmental Protection Agency, Accessed March 20, 2023,

https://www.epa.gov/climateleadership/ghg-inventory-development-process-and-guidance.

20 “California Climate Action Registry,” Climate Action Reserve, Accessed March 10, 2023, California Climate Action Registry – Climate Action Reserve : Climate Action Reserve.

21 “2019 Refinement to the 2006 IPCC guidelines for National Guidelines for National Greenhouse Gas Inventories,” IPCC, Accessed March 17, 2023, https://www.ipcc.ch/site/assets/uploads/2018/05/1506_Summary_TA-EIW-1.pdf.

22 “2019 Refinement to the 2006 IPCC guidelines for National Guidelines for National”, Greenhouse Gas Inventories, Accessed on March 20, 2023, https://www.ipcc.ch/report/2019-refinement-to-the-2006-ipcc-guidelines-for-national-greenhouse-gas-inventories/#:~:text=The%202019%20Refinement%20was%20not,with%20the%202006%20IPCC%20Guidelines.

23 “The Roadmap to More Interoperable Greenhouse Gas Emissions Accounting,” The Carbon Call, Climate Works Foundation, November, 2022, https://carboncall.org/news/the-roadmap-to-more-interoperable-greenhouse-gas-emissions-accounting/.

24 Liu Zheng, Quigshan Qian, Bin Hu, Wen Long Shang, Lingling Li, Yuanjun Zhao, Zhao Zhao, Chinjia Han et al., “Government regulation to promote coordinated emission reduction among enterprises in the green supply chain based on evolutionary game analysis,” Elsevier, 106290, https://www.sciencedirect.com/science/article/abs/pii/S0921344922001380.

25 Kaplan, Robert S. and Karthik Ramanna, “Accounting for Climate Change,” Harvard Business Review, November-December 2021, https://hbr.org/2021/11/accounting-for-climate-change

26 “Challenges when calculating scope 3 emissions,” Claims Carbon Institute, Accessed March 31, 2023,

https://claimscarbon.com/2022/02/02/challenges-when-calculating-scope-3-emissions/.

27 Cannon, Charles, Suzanne Greene, Thomas Koch Blank, Jordy Lee, and Paolo Natali, “The Next Frontier of Carbon Accounting: A Unified Approach for Unlocking Systemic Change,” Rocky Mountain Institute, 2020, https://rmi.org/wp-content/uploads/2020/06/The-Next-Frontier-of-Carbon-Accounting-June-2020.pdf.

28 Kaplan and Ramanna, “Accounting for Climate Change”

29 George, Sarah, “Carbon Call’: 20 major players including Microsoft team up to improve emissions accounting,” Edie Newsroom, February 11, 2022, https://www.edie.net/carbon-call-20-major-players-including-microsoft-team-up-to-improve-emissions-accounting/.

30 Claims Carbon Institute, “Challenges when calculating scope 3 emissions,”

31 “Recommendations of the Task Force on Climate-related Financial Disclosures,” Task Force on Climate-Related Financial Disclosures, June 15, 2017, https://assets.bbhub.io/company/sites/60/2021/10/FINAL-2017-TCFD-Report.pdf.

32 “5 Ways the G20 Can Support Climate Action and Sustainable Development.” World Resources Institute. Accessed May 12, 2023.

https://www.wri.org/insights/5-ways-g20-can-support-climate-action-and-sustainable-development.

33 “Climate crisis: UN chief calls on G20 to take ‘bold decisions and actions.”, United Nations News., November 14, 2022. Accessed May 13, 2023. https://news.un.org/en/story/2022/11/1130557.

34 “Closing the Gap: The Impact of G20 Climate Commitments on Limiting Global Temperature Rise to 1.5°C”, Climate Analytics and World Resources Institute, September 2021. Accessed May 12, 2023. https://files.wri.org/d8/s3fs-public/2021-09/closing-the-gap-impact-g20-climate-commitments-limiting-global-temperature-rise-1-5c.pdf?VersionId=RlUJyvgmgnudRbZDDTG_x_nzcG57JMWd.