Task Force 4 Refuelling Growth: Clean Energy and Green Transitions

Abstract

The trucking sector plays a critical role in a country’s economy. Globally, trucks account for only 4 percent of the on-road fleet but are responsible for 27 percent of greenhouse gas emissions (MacDonnell and Façanha, 2021). In developing nations, trucking demand is growing steadily, driven by the increase in economic output. Zero-emission trucks (ZETs) are a compelling alternative to diesel trucks, lowering operating costs and environmental impact. However, the nascent ZET market faces key challenges, such as the lack of demand and supply, limited infrastructure, and dearth of affordable finance and supportive policies.

This policy brief highlights the strategies to fast-track ZET adoption in developing nations. It proposes formulating relevant policies and adopting ambitious targets for ZETs, underlining the need for concerted efforts towards a robust ZET supply chain. The brief also proposes ways to mobilise finance, deploy suitable charging/refuelling infrastructure, and promote research innovation and knowledge exchange to foster the ZET ecosystem in the G20 countries and the developing world.

The Challenge

The trucking sector is central to a country’s economic growth and fulfils the daily needs of businesses and consumers. Globally, medium- and heavy-duty trucks represent only 4 percent of the on-road fleet but are responsible for 27 percent of the greenhouse gas emissions and 60 percent of the global nitrogen oxide (NOx) emissions from the road sector (MacDonnell and Façanha, 2021). This will be more prominent in developing economies[a] as their trucking activity increases with rising economic activities (International Energy Agency, 2017). As trucks rely primarily on diesel fuel, a surge in trucking activity will increase CO2 emissions, air pollution, and operating costs.

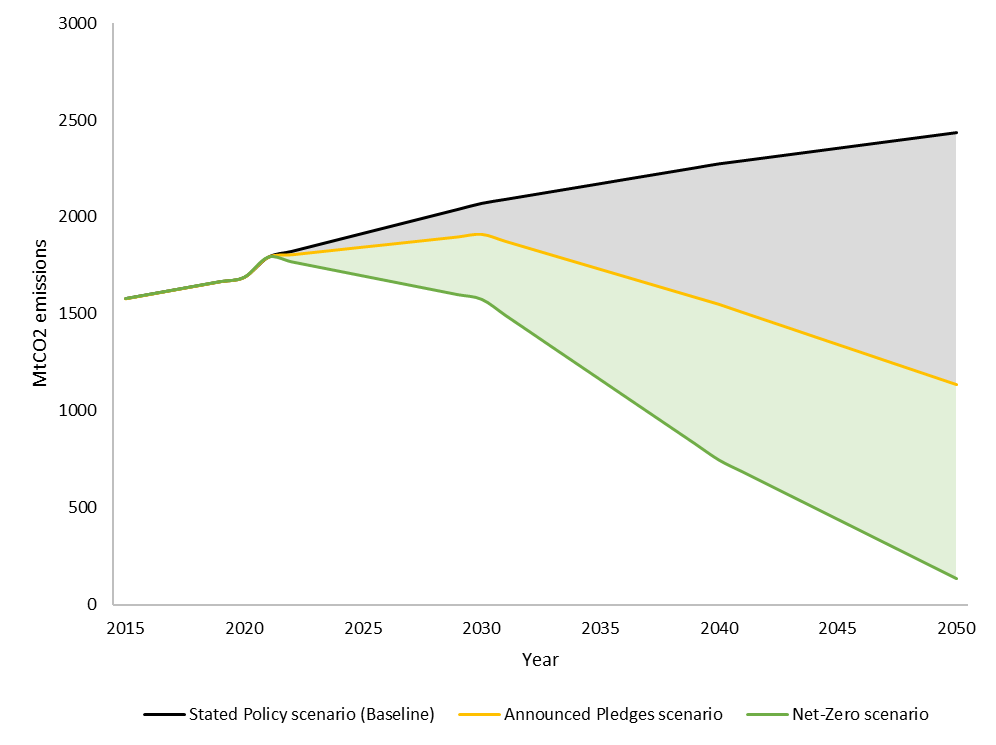

Zero-emission trucks (ZETs) offer a compelling solution to the growing challenges associated with the conventional trucking sector. They are more efficient than diesel trucks, do not emit harmful pollutants from tailpipes (such as particulate matter and NOx), and have lower CO2 emissions (depending on vehicle type and electricity grid mix) and operating costs. Meeting global climate commitments requires the world reaching net-zero by 2050, which is far-fetched without ZETs achieving a 100 percent share in new sales. Globally, in a net-zero scenario,[b] ZETs can help mitigate more than 36 Gt CO2 cumulatively in the 2022-50 period compared to the stated policy scenario (baseline) (see Figure 1) (International Energy Agency, 2022c).

Figure 1: Global CO2 emissions from medium- and heavy-duty trucks

Source: IEA’s World Energy Outlook (International Energy Agency, 2022c)

Transportation cost is one of the key components of overall logistics costs. Reducing transportation costs through ZETs can significantly lower logistics costs, which is crucial for developing countries where logistics costs can make up a large portion of the GDP. In India, Indonesia, and Brazil, logistics costs account for 14 percent, 23 percent, and 12 percent of the GDP, respectively, which is much higher than the 8 percent-10 percent average in developed nations (Santoso et al., 2021; NITI Aayog, RMI and RMI, 2021; FGV Transportes, 2020). ZET adoption in India could reduce this share to 11.5 percent, leading to significant fuel cost savings (Sinha and Teja, 2022). This will be contingent upon declining costs of green hydrogen and batteries, the expansion of renewable electricity grid, the development of green hydrogen infrastructure, and the increased availability of ZET models.

While ZETs provide a sustainable alternative to diesel trucks, some key barriers could inhibit their uptake in developing nations. The ZET market in most developing economies is nascent, with limited or no ZET models. Of all the medium and heavy ZET models available globally in 2022, 92 percent were in China, North America, and Europe; India and Mexico contributed to 5 percent of the total availability, while there were limited or no ZET models available across the rest of the developing world (Global Commercial Vehicle Drive to Zero, 2022). Long-term policy signals and associated incentives to promote ZETs are lacking in most developing nations (Khan et al. 2022). This could disincentivise demand-side players from purchasing more expensive ZETs over diesel trucks.

Furthermore, the lack of a dense network of charging and refuelling stations and power access for charging limits the operational feasibility of ZETs (International Energy Agency, 2022d). Moreover, there is a lack of reliable electricity supply in emerging economies in Africa (World Economic Forum, 2021). Renewables penetration (solar and wind) in Africa and Southeast Asia is also low, accounting for 4 percent of their total electricity generation (International Energy Agency, 2022c). Similarly, low-carbon hydrogen’s share in total hydrogen production globally is just around 1 percent (International Energy Agency, 2023a). Lastly, financiers are sceptical about zero-emission vehicle technology performing at par with internal combustion engine counterparts, leading to increased costs of borrowing and limited access to debt financing (International Energy Agency, 2021). See Figure 2 for more details on the challenges in creating the ZET ecosystem in developing countries.

Figure 2: Key challenges related to ZET adoption in developing nations

Source: Authors’ compilation

The G20’s Role

The G20 nations represent 85 percent of the global GDP and 75 percent of the global trade (G20 India, 2023). As such, the G20 is central to issues related to freight and trucking decarbonisation. As an international forum to align on economic cooperation between regions, the G20 can act as an anchored pillar to encourage and facilitate global efforts towards the ZET transition.

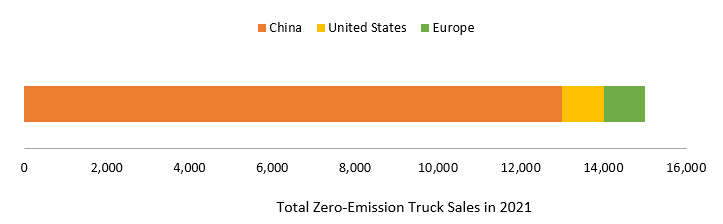

Certain G20 nations have started to realise the benefits of switching to ZETs. Countries like China and the US have begun introducing policies and mandates to enable the transition, which has led to an increase in ZET sales from 5,000 in 2020 to 15,000 in 2021 (see Figure 3) (International Energy Agency, 2023). In most developing countries, the sale and adoption of ZETs have been limited (Khan et al. 2022). The G20 presents an opportunity for cross-learning and collaboration to fast-track ZET deployment. Developing countries can incorporate learnings from nations that have started to deploy ZETs and associated charging technology and business models.

Figure 3: Zero-emission truck sales in the US, China, and Europe in 2021

Source: Authors’ compilation based on International Energy Agency (2023)

Fostering the ZET ecosystem

Zero-emission trucks cut across different G20 nations’ priorities, such as energy transition, emissions mitigation, trade, finance, and green growth. Recognising the need for research and innovation, financing, and market creation to enable a ZET transition in the developing world, the G20 can create several avenues for innovation, cross-collaboration and driving commitments:

- Market creation: The G20 can create a global narrative on the urgency and need for switching to ZETs and generate awareness around the environmental and economic benefits. This will instil confidence in policymakers and industry players towards the ZET transition and initiate a necessary demand pull for ZETs. Furthermore, the G20 can create a compendium of policy recommendations and financing solutions to facilitate the manufacturing and adoption of ZETs and promote the creation of a global market for renewable energy and green hydrogen.

- Facilitating stakeholder collaboration: The ZET value chain is vast and spans a myriad of stakeholders and their interests and priorities. The G20 can facilitate a multinational forum to start collaborative discussions among different stakeholder groups. Stakeholders could include:

- Policymakers aiming to make the trucking sector more efficient in line with their geography’s economic and environmental goals.

- Automakers trying to increase their market share by selling high-performing, reliable, and clean vehicle alternatives.

- Fleet operators ensuring they can cost-effectively move goods with the least environmental impact.

- Truck owners trying to minimise their fuel expenditure.

- Charging/hydrogen refuelling station operators trying to maximise the utilisation of their assets.

- Electricity providers ensuring a reliable supply of power.

- Financiers providing affordable financing solutions for ZETs.

Concerted efforts by different stakeholders in tandem will foster the ZET ecosystem.

- Steering research and innovation: Technological innovation is the key to bringing down the cost of ZETs, reducing reliance on critical minerals, decreasing the charging time, and enhancing the efficiency of ZETs. The G20 can promote research in sustainable mineral exploration, processing, and recycling to increase the availability of critical minerals. In addition, it can facilitate research in co-developing new battery chemistries, building energy-efficient ZETs, and promoting global standards for charging infrastructure.

- Sharing best practices and learnings: The ZET transition can be accelerated by sharing learnings and experiences from the deployment of early ZET pilots within some G20 nations. The G20 can provide a platform to share such learnings through its discussion forums, touching upon challenges and solutions related to ZET manufacturing, technology, charging/refuelling, financing, and related policies. Cross-learning will enable developing nations to avoid any pitfalls as they plan the near- and long-term deployment of ZETs.

Recommendations to the G20

Creating a compendium of policy best practices

Policies play a key role in accelerating electric vehicle (EV) adoption across the globe. The G20 can develop a compendium of best practices for ZET policies to inspire governments to introduce suitable policy measures in their respective countries. The compendium can include a menu of demand- and supply-side policies and global case studies to inform the design and implementation.

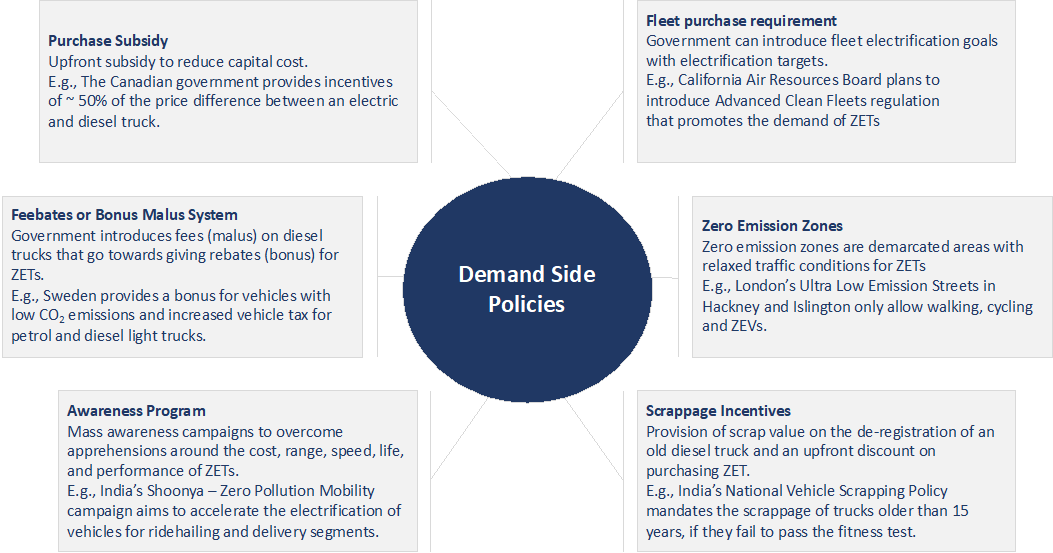

Demand-side policies (such as purchase subsidies, rebates, and tax and toll exemptions) can lay the foundation for the ZET market and encourage industry players to adopt ZETs (see Figure 4). Non-fiscal incentives, such as priority parking and access to zero-emission zones, can ease the operation of ZETs.

Figure 4: Demand-side strategies to catalyse ZET adoption

Source: Authors’ compilation

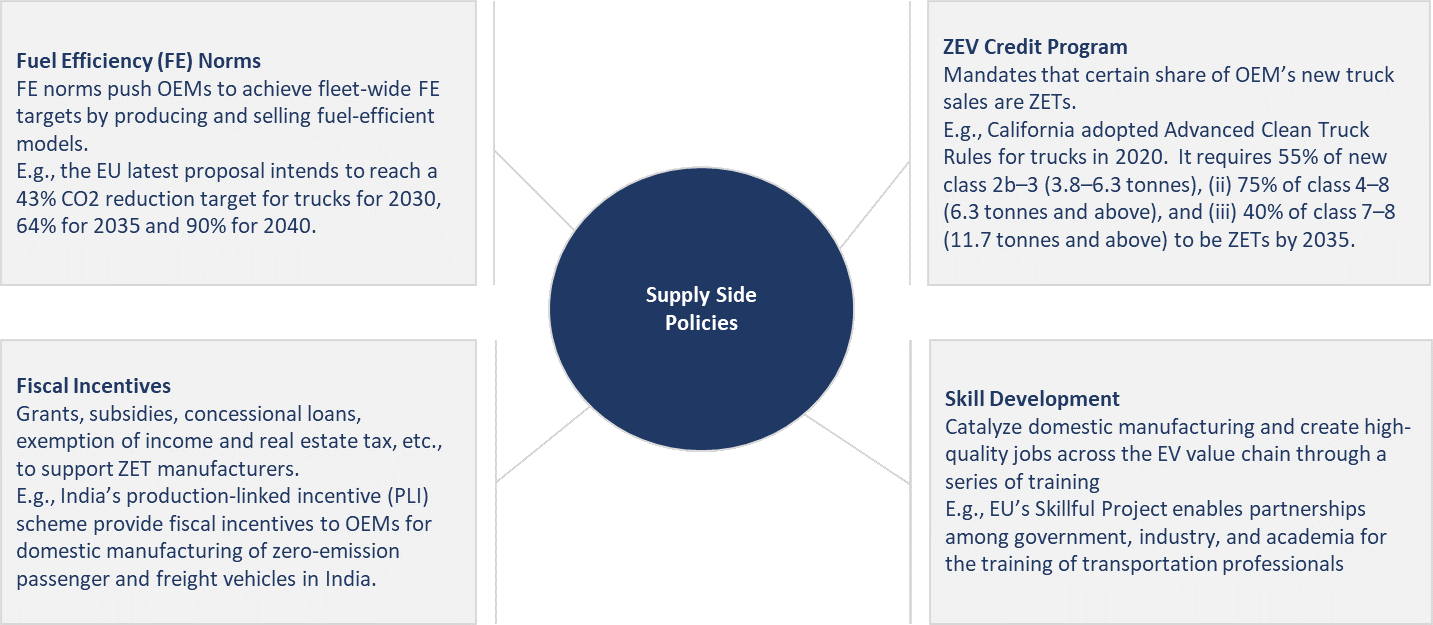

Moreover, fleet purchase requirements can ensure fleet operators adopt ZETs, thus creating an initial market for manufacturers. Supply-side incentives, such as grants and tax exemptions, can encourage traditional auto manufacturers and startups to venture into the ZET space (see Figure 5). Measures such as the ZEV credit programme and fuel economy norms can increase the availability of ZET options in the market. In addition, training and skilling programmes can ensure the availability of the capacity and capabilities required to smoothen the ZET transition.

Figure 5: Supply-side strategies to foster ZET manufacturing

Source: Authors’ compilation

Adopting ambitious joint targets to spur deployment of ZETs and necessary infrastructure

Targets can play a key role in creating an EV ecosystem. Considering the quantum of investments required in ZET manufacturing, targets and enabling government policies can build the confidence of original equipment manufacturers (OEMs) to invest in ZET research and development. Target announcements can also help fleet, logistics service providers, and e-commerce companies plan long-term decarbonisation strategies and set ZET deployment goals. Moreover, long-term targets and policy roadmaps for transitioning to ZETs can help investors build their confidence in large investments in the ZET ecosystem.

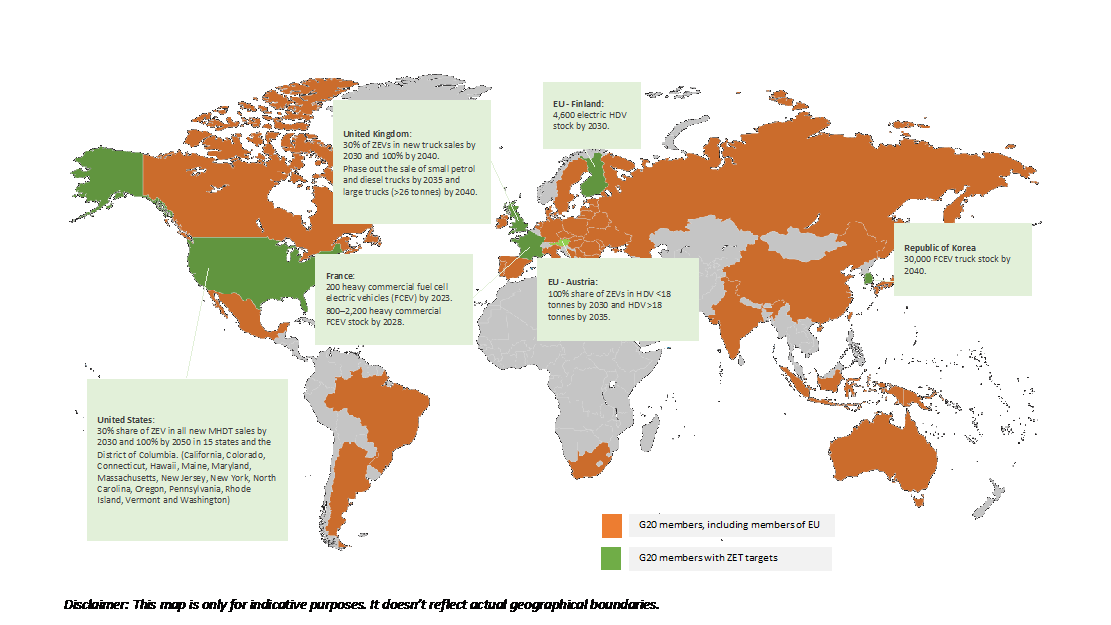

Some geographies have started announcing their ZET electrification targets (see Figure 6). The G20 can further accelerate this by calling for a clear and common near- and long-term target for ZETs worldwide.

Figure 6: Electric truck targets by different countries

Source: Authors’ compilation from International Energy Agency (2022a) and Wappelhorst and Rodríguez (2021)

Facilitating the development of a robust supply of ZETs and promoting circularity for ZET components

To increase the ZET model availability and ramp up production of vehicles, automakers need to innovate, collaborate on technology development, and invest in dedicated production facilities to achieve scale and reduce costs. To further enhance the supply of ZETs, a focus on ensuring the availability of essential minerals and battery and fuel cell components is critical. The majority of this supply chain is concentrated in a few regions across the globe (International Energy Agency 2022b). A focus on circularity and recycling of these materials and components can help diversify the supply chains and mitigate risks related to raw material availability and costs.

The G20 can take the following actions to create an effective supply chain ecosystem that can enhance ZET manufacturing:

- Host a forum for global truck OEMs: The G20 can host a forum inviting leading automakers and fleet operators across G20 nations to share their perspectives, plans, and solutions to enhance ZET model availability. Such a platform could pave the way for partnerships among different OEMs, and between OEMs and fleet operators to co-develop new technologies and produce fit-to-purpose ZETs. These partnerships can enable scale and reduce the costs of manufacturing ZETs and associated components, helping the OEMs produce cost-effective ZET models.

- Enhance circular economy and recycle materials: The G20 can also focus on enhancing the circular economy, especially through recycling batteries, fuel cell components, and associated materials. This can reduce the burden of mining and component manufacturing. The G20’s working group on environment and climate sustainability, which currently focuses on the circular economy along with other areas, can include discussions on circularity and recycling pathways for ZET components(G20 India 2023).

Spurring action to support widespread charging and refuelling infrastructure

Typically, ZETs haul heavy loads over long distances, translating to a significant battery pack and hydrogen fuel tank capacity for battery electric trucks (BETs) and fuel cell electric trucks (FCETs), respectively. A robust infrastructure network is essential to satisfy the high power and energy requirements of ZETs. Different technologies and projects are being deployed to charge BETs globally. These include plans for the electrification of a 2100 km long I-5 Interstate Corridor for medium and heavy trucks in the US (West Coast Clean Transit Corridor Initiative, 2022), uptake of battery-swappable trucks in China (Yukun, 2023), and the demonstration of catenary-based charging in Germany (Ewing, 2021). peak power demand from BETs, especially for long-haul use cases, can be very high, requiring a supporting upstream electricity grid network. Meanwhile, demonstrations have kickstarted for refuelling of FCETs. The H2Haul project funded by the European Union includes high-capacity refuelling stations for 16 FCETs (European Commission, 2019).

To accelerate the deployment of infrastructure assets, the G20 can facilitate partnerships by creating platforms for connections among governments, financiers, and industries for sharing best practices and technical know-how regarding different charging/refuelling strategies. The G20 can also promulgate shared principles for the rapid scaling of upstream power grid infrastructure to support the high-power requirements of trucks, and host discussions on the need for a global green hydrogen market. Furthermore, it can form mutual targets for developing electric/hydrogen corridors, standardise infrastructure, and ensure interoperability. Finally, the G20 can take the lead in communicating the need and urgency of infrastructure deployment worldwide to ensure ZET adoption. See Figure 7 for more details on strategies to spur infrastructure deployment are presented below:

Figure 7: Strategies to promote the deployment of supporting infrastructure for ZETs

Source: Authors’ compilation

Mobilising finance to scale ZET and infrastructure deployment

Automakers require considerable investments in laying new supply chains or retrofitting existing ones to manufacture ZETs, and thus need financing support to manufacture ZETs. In terms of adoption, truck retail financing is currently perceived as a high risk due to its nascent nature, and lack of performance history, established residual value and supporting charging ecosystem (Sinha and Teja, 2022).

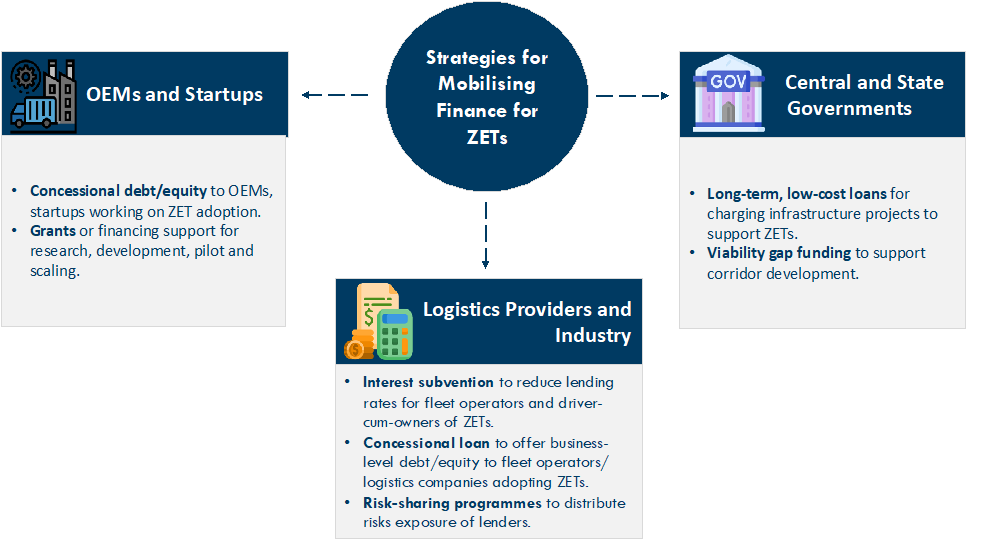

The G20 can convene multilateral development banks (MDBs) and development financial institutions (DFIs) to provide blended finance that uses public capital to underwrite the risks associated with the ZET market and attract commercial investors. MDB capital can support national/state governments to create the necessary charging and refuelling infrastructure for the ZETs through long-term, low-interest loans. Additionally, DFIs can play an active role in providing debt capital at concessional terms to promising ZET OEMs and startups. Bilateral development agencies from the G20 countries can also provide early-stage research and development grants to nurture upcoming ZET-focused startups. Furthermore, to fulfil the need for affordable financing options for fleet and owner-operators, MDBs can offer partial risk-sharing guarantees and concessional loans to local banks and financiers. Finally, the G20 can create a compendium of strategies that the development banks can leverage to support the financing needs of governments, OEMs, logistics operators and industry (see Figure 8).

Figure 8: Strategies to mobilise finance for ZETs

Source: Authors’ compilation

Convening discussions on policies and technological innovation for capacity support and knowledge exchange

The G20 can support collaborative efforts across countries to enhance ZET technology innovation, support demonstration projects, and provide a stage for developing nations to share knowledge and best practices related to ZET adoption.

- Advancing technology innovation: To promote innovation in ZET technology, the G20 can encourage competition on new and upcoming technologies in vehicles, associated infrastructure, advanced cell chemistry batteries and next-generation fuel cells among major companies—both legacy and startups—in the G20 countries. The competition can be targeted at innovating low-cost solutions for application.

- Facilitating knowledge exchange: The G20 can host discussions with developing countries to share best practices about ZET operations and on case studies to inform the design of ZET policies. It can further form working groups, including expert stakeholders from the ZET ecosystem, to provide capacity support to these countries.

- Promoting pilots: The G20 can promote demonstration projects to test the operational and economic viability of new ZET technologies across various use cases. Committees can be formed within the G20 cohort to capture the learnings from the pilots, which can be shared publicly in forums and events.

- Fostering inclusion: The G20 can advocate for increased partnerships with developing countries in various international forums related to ZETs and related infrastructure. Providing a platform for developing nations to address their challenges and concerns can foster effective collaboration among stakeholders across different nations.

Conclusion

The accelerated adoption of ZETs in the G20 countries and other developing nations is paramount to achieving the climate goals, reducing air pollution, and making the logistics sector more efficient. The G20’s role in addressing critical issues on economic cooperation, climate, and trade provides an opportunity for this coalition to serve as a leading voice for the ZET transition. The G20 can leverage some of its member countries’ strengths, experiences, and learnings in leading the ZET transition and create avenues for other developing nations to draw upon these learnings. It can create a demand pull for ZETs by developing channels for cross-learning, enhancing effective multistakeholder collaboration, and spearheading innovation and research efforts.

Overall, focusing on enabling policies, mutual target setting, enhancing supply chains for ZET manufacturing, spurring infrastructure deployment, enabling access to finance and promoting knowledge exchange can help foster a global ZET ecosystem. Collective efforts spearheaded by the G20 can help decarbonise medium and heavy-duty vehicles worldwide.

Attribution: Akshima Ghate et al., “Promoting Zero-Emission Trucking Across Developing Nations,” T20 Policy Brief, May 2023.

Bibliography

European Commission. “Hydrogen Fuel Cell Trucks for Heavy-Duty, Zero Emission Logistics.” Last Updated January 7, 2023. Global Commercial Vehicle Drive to Zero.

Ewing, Jack. “What if Highways Were Electric? Germany Is Testing the Idea.” The New York Times, August 3, 2021.

G20 India. “G20 – Background Brief.” 2023.

Global Commercial Vehicle Drive to Zero. “ZETI Data Explorer.” 2022.

FGV Transportes. “Overview of the Logistics Sector in Brazil.” November 2020.

International Energy Agency. “Towards Hydrogen Definitions Based on Their Emissions Intensity.” April 2023a.

International Energy Agency. “Electric Truck Registrations and Sales Shares by Region, 2015-2021.” Accessed March 29, 2023b.

International Energy Agency. “Global EV Policy Explorer Key policies and Measures that Support the Deployment of Electric and Zero-Emission Vehicles.” Last modified May 23, 2022a.

International Energy Agency. “Global Supply Chains of EV Batteries.” Last modified July 2022b.

International Energy Agency. “World Energy Outlook 2022.” Last modified October 2022c.

International Energy Agency. “Global EV Outlook 2022.” May 2022d.

International Energy Agency. “Financing Clean Energy Transitions in Emerging and Developing Economies.” June 2021.

International Energy Agency. “The Future of Trucks.” June 2017.

Khan, Tanzila, Yang, Zifei, Kohli, Sumati, and Miller, Josh. “A Critical Review of ZEV Deployment in Emerging Markets.” The International Council on Clean Transportation. (February 2022).

MacDonnell, Owen, and Façanha, Cristiano. “How Zero-Emission Heavy-Duty Trucks can be Part of the Climate Solution.” Calstart, December 2, 2018.

NITI Aayog, RMI, and RMI India. “Fast Tracking Freight in India.” June 2021.

Santoso, Sugeng, R. Nurhidayat, Mahmud, Gustofan, and Arijuddin, Abdul Mujib. “Measuring the Total Logistics Costs at the Macro Level: A Study of Indonesia.” Logistics, 5(4) (October 01, 2021): 68.

Sinha, Sudhendu, and Teja, Joseph. “Transforming Trucking in India: Pathways to Zero-Emission Truck.” NITI Aayog, RMI. Last modified September 2022.

Wappelhorst, Sandra, and Rodríguez, Felipe. “Global Overview of Government Targets for Phasing Out Internal Combustion Engine Medium and Heavy Trucks.” The International Council on Clean Transportation. Last modified August 26, 2021.

West Coast Clean Transit Corridor Initiative. “West Coast Clean Transit Corridor Initiative Study Fact Sheet”. June 2020.

World Economic Forum. “Fostering Effective Energy Transition 2021 edition.” April 2021.

Yukun, Liu. “Battery Swapping Key for Heavy-Duty Ttrucks.” China Daily, January 18, 2023.

[a] Based on the United Nations’ classification of ‘developing economies’. For the full list.

[b] As per the International Energy Agency’s assessment, the stated policy scenario (baseline) considers today’s policy settings, the announced pledge scenario assumes all government announcements and targets are timely met, and the net-zero scenario assumes new sales of internal combustion engine trucks to cease by 2045 to achieve the global 1.5°C target.